ecommerceSeo#DTC ecommerce#ecommerce stack#multi-market ecommerce#AI SEO#Google Shopping#structured product data

How Should Multi-Market DTC Brands Choose an Ecommerce Stack in 2026?

This guide reframes ecommerce stack selection around what matters now for DTC brands: acquisition efficiency, structured product data, localization, channel sync, and AI-era discoverability.

How Should Multi-Market DTC Brands Choose an Ecommerce Stack in 2026?

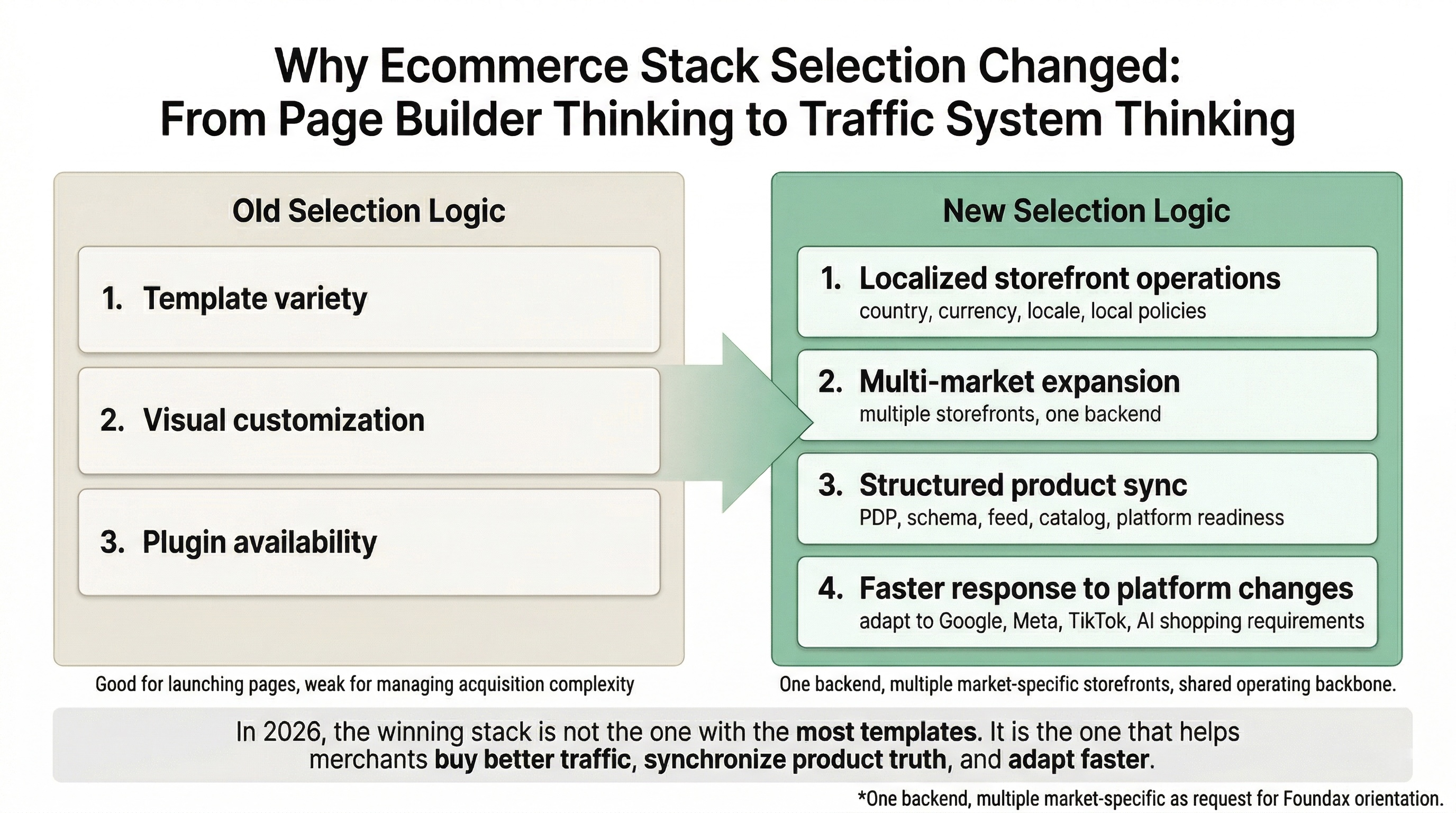

If you still evaluate ecommerce platforms mostly by asking how many templates they have, how customizable the pages look, or how many plugins you can install, you are using an outdated lens.

In 2026, the question is no longer whether a tool can help a DTC brand launch a storefront.

The real question is whether it can help you keep acquiring external traffic efficiently when:

traffic costs are elevated and volatile

distribution is increasingly automated

Google, Meta, TikTok, ChatGPT, and Google AI Mode all depend more heavily on machine-readable product data

That is why platform selection is no longer just a site-building decision.

It is now a traffic-systems decision.

The strongest ecommerce platform in 2026 is not simply the one that helps you design pages fastest. It is the one that helps you buy precise traffic, synchronize structured product data, capture organic and AI discovery, and adapt quickly as platform rules change.

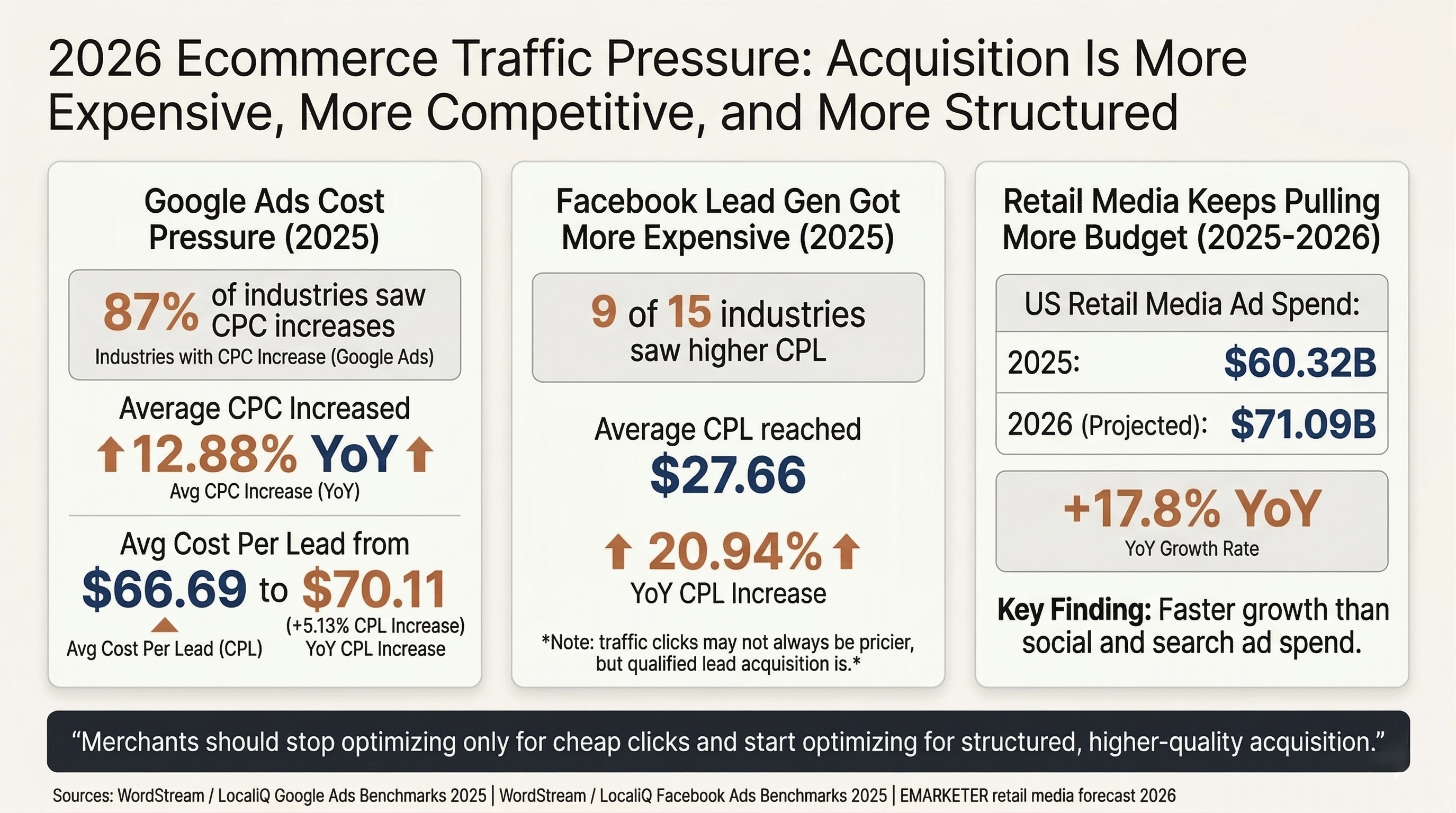

Effective acquisition costs in Google Ads and Facebook Lead Ads are still rising, while retail media budgets continue to expand.

1. Why platform choice changed in 2026

Independent ecommerce merchants still rely on the same broad acquisition buckets:

Paid Search

Paid Social

Creator and affiliate traffic

Marketplace spillover

SEO and AI discovery

Owned channels like email and SMS

What changed is the pressure on each layer.

Higher-quality acquisition is more expensive and less forgiving

Recent benchmark data makes the pattern clear:

WordStream / LocaliQ's 2025 Google Ads Benchmarks found that 87% of industries saw CPC increases in Google Ads, while average CPC rose 12.88% year over year. For most categories, buying the click itself did not get easier. WordStream / LocaliQ Google Ads Benchmarks 2025

The same benchmark shows average CPL rising from $66.69 to $70.11, a 5.13% year-over-year increase. That is a more commercially meaningful signal than CPC alone because it is closer to what merchants actually pay for a usable lead. WordStream / LocaliQ Google Ads Benchmarks 2025

WordStream / LocaliQ's 2025 Facebook Ads Benchmarks reports that Facebook leads campaigns saw average CPL rise 20.94% to $27.66, with 9 of 15 industries posting higher CPL. Even when some traffic metrics fluctuate, qualified acquisition can still get more expensive. WordStream / LocaliQ Facebook Ads Benchmarks 2025

EMARKETER forecasts US retail media ad spend at $60.32B in 2025 and $71.09B in 2026, a 17.8% increase. Brands are still pushing more budget into commerce-linked media rather than backing away from paid acquisition. EMARKETER 2026 Retail Media Forecast

Tinuiti's 2026 retail media outlook reinforces the same direction: retail media remains one of the fastest-growing segments in digital advertising, which means merchants are being pushed toward channels that depend more on structured product inputs and closed-loop measurement. Tinuiti 2026 Outlook

The implication is not that every metric rises in a straight line.

It is that higher-quality acquisition has become more expensive, while the broader acquisition environment has also become more volatile, more fragmented, and more dependent on structured product inputs.

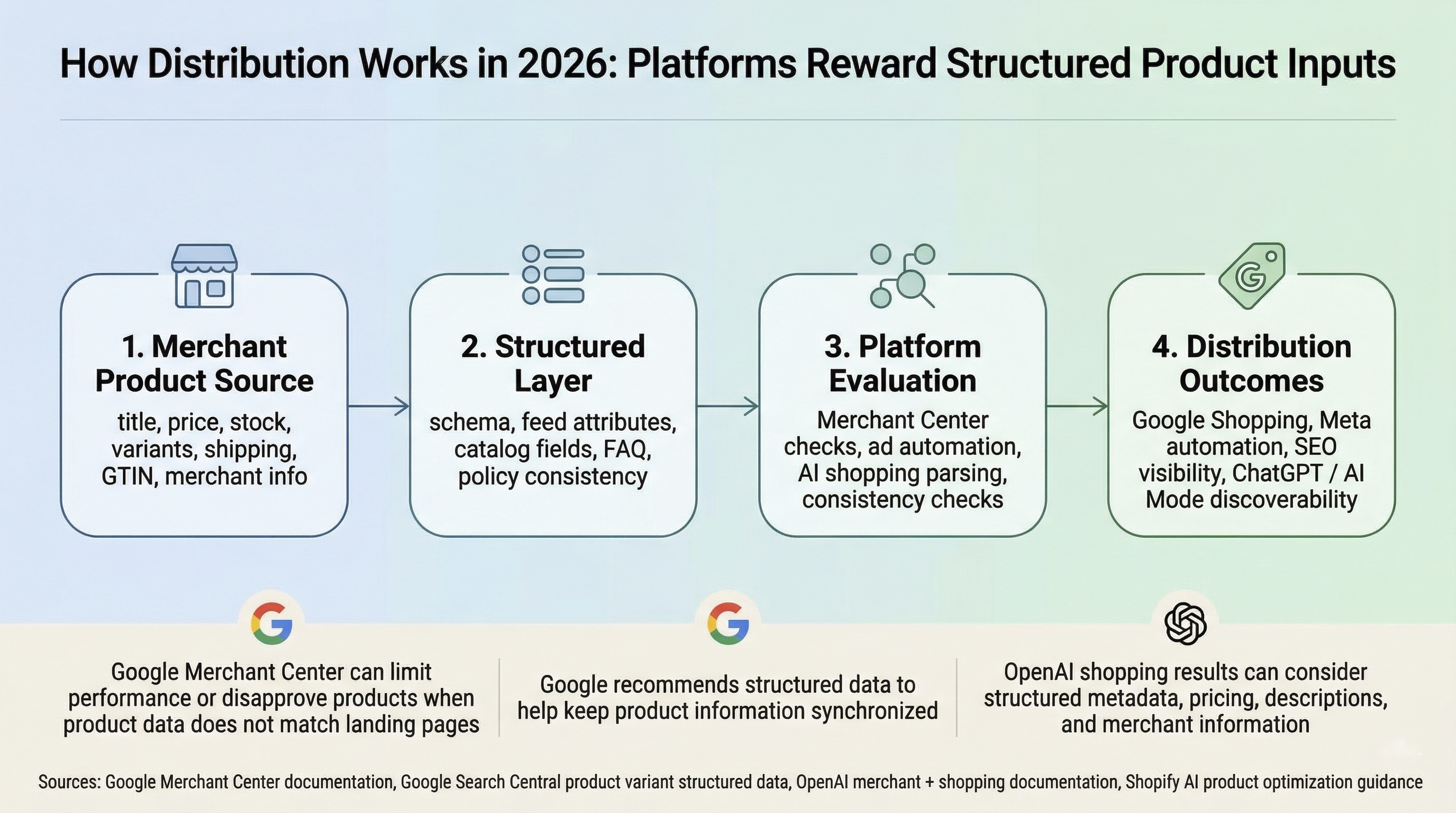

Distribution is becoming more product- and feed-driven

Platforms are also shifting away from manual targeting logic toward machine-led product distribution.

The operating loop is increasingly straightforward: cleaner merchant product inputs feed cleaner structured layers, which lead to better platform evaluation and better distribution outcomes.

Tinuiti reported that Advantage+ Shopping Campaigns reached 38% of Meta retail ad spend in Q1 2025, up from 24% a year earlier. Tinuiti Q1 2025

By Q3 2025, Performance Max accounted for 68% of Google Shopping listings spend among retailers running both campaign types. Tinuiti Q3 2025

Google Merchant Center warns that when submitted product data does not match the website, products may be disapproved or continue to show with limited performance, including lower impressions and clicks. Google Merchant Center: product data quality violations

Google also recommends structured data when using automatic item updates so site data and Merchant Center data stay aligned. Google Merchant Center: stay approved

In other words, the ad platform increasingly wants structured product truth, not just creative and audience inputs.

AI shopping entry points are no longer theoretical

OpenAI, Google, and Shopify have all made this shift explicit:

OpenAI now lets merchants participate in ChatGPT product discovery through product feeds. OpenAI merchants

OpenAI says ChatGPT shopping can consider structured metadata, pricing, descriptions, and merchant information. Shopping with ChatGPT Search

Google introduced AI Mode shopping in May 2025 and highlighted the scale and refresh frequency of the Shopping Graph. Google, May 20 2025

In March 2026, Google expanded more personalized shopping recommendations in the U.S. Google, Mar 17 2026

Tinuiti’s Q1 2026 AI Citation Trends Report already tracks ChatGPT, Google AI Mode, Google AI Overviews, Gemini, Copilot, and Meta AI in one citation framework. In January 2026, social media accounted for 9% of total citations, and social content was cited more than 4x as often by AI Overviews as by Gemini. Tinuiti Q1 2026 AI Citation Trends

Shopify now has official guidance on optimizing products for AI platforms, including titles, images, product organization, variants, barcodes, and FAQs. Shopify: Optimizing your products for AI platforms

That means merchants are no longer choosing a platform just for storefront delivery.

They are choosing the system that determines whether their catalog can be understood well enough to earn distribution.

2. Why merchants now need precision, not just more spend

When traffic gets more expensive and platforms become more automated, the answer is not simply “buy more traffic.”

The answer is to make each unit of traffic more precise and more efficient.

That depends on infrastructure, not just campaign tactics.

Merchants increasingly need:

region-specific storefronts that match region-specific traffic

cleaner structured product data

tighter consistency between PDPs, feeds, structured data, and policy content

stronger organic and AI discoverability to offset paid pressure

That is why a lot of “media buying problems” are actually platform problems in disguise.

3. The 3 platform questions that matter more than template variety

The more durable 2026 growth loop is not “launch first, patch SEO later, add plugins later.” It is “build market-specific sites, structure product truth, synchronize channels, and let that same data support ads, SEO, and AI discovery.”

1) Can the platform support localized regional operations and multi-market expansion at the same time?

If you want more precise traffic, each market should usually have a clearer operational surface:

language

pricing and currency

tax and shipping promises

local FAQs and policy content

But if every new market means a new disconnected stack, operations become unmanageable.

That is why the real requirement is not “one site that awkwardly covers the world.”

It is “market-specific storefronts with centralized backend control.”

Foundax is relevant here because it already models site creation around marketCountry, currency, and enabled locales, while letting one account manage multiple websites from the same backend.

2) Can the platform connect cleanly to media platforms and synchronize structured product data?

This is where many stacks become too plugin-dependent.

Google’s own docs make the stakes clear:

mismatched product data can reduce impressions or trigger disapprovals

pricing, sale windows, shipping, GTIN, and other product attributes matter

Merchant API attributes now extend into more detailed structured product representations

Foundax’s current product implementation matters because it exposes this operational layer directly:

site-level SEO Workspace for publication state, primary domain, Google connection, Search Console, GMC preflight, and sync state

product-level SEO Workbench for source mapping, required checks, suggested checks, suppression, JSON-LD, GMC payloads, and Dry-run diffs

site-level ads conversions workspace for Google, Meta, and TikTok connection, verification, strategy control, and delivery visibility

That is much more useful than a vague “Google integration supported” claim.

3) Can the platform help you capture natural demand and increase recognition by Google Shopping and AI systems?

Merchants cannot rely on paid acquisition alone.

Google Search Central has long been explicit that variant relationships such as ProductGroup, variesBy, and hasVariant are critical for machine understanding. Google Search Central: Product variants

Foundax already supports the building blocks needed for this layer:

language-specific page SEO configuration

runtime injection of metadata including canonical and alternates

server-rendered Product JSON-LD on PDPs

dynamic robots.txt and sitemap.xml output tied to published and accessible pages

That combination is operationally important because the same structured truth supports both paid and organic visibility.

4. Why choosing a tool now means choosing an adaptation engine

In 2026, templates and visual customization are getting easier to generate.

That is not where the long-term advantage lives.

The harder part is whether your platform can keep up when Google, Meta, TikTok, ChatGPT, and other surfaces change how they evaluate merchants, products, and feeds.

That is why merchants should now ask:

Can this platform support market-by-market site operations?

Can it keep product data synchronized across website, feed, and structured output?

Can it support ads, SEO, and AI discovery using the same source of truth?

Can it productize new platform requirements quickly, instead of forcing merchants back into plugin stacking and custom patches?

Why Foundax becomes more relevant in that environment

The strongest reason to look at Foundax is not page aesthetics.

It is that Foundax is being built as an AI-native SaaS workflow rather than as a traditional CMS plus plugin pile:

SEO, product data, content, and sync workflows are being designed as one operating loop

merchants can inspect what machines are actually reading

AI capabilities are already embedded into Builder and Content Studio workflows, rather than bolted on as a separate helper

That matters because in the next wave of ecommerce infrastructure, the winning platforms will not be the ones with the longest theme marketplace.

They will be the ones that can turn changing platform requirements into merchant-usable workflows fast enough.

The most important ecommerce platform question in 2026 is no longer “Can I build a unique site?” It is “Can this system keep my acquisition engine aligned with how discovery platforms now work?”

Why can’t brands choose an ecommerce platform in 2026 by looking only at templates and the editor?

Because templates and editors mainly answer “can we build it?” The harder 2026 question is whether the platform can absorb traffic, distribute products, and support acquisition, search, and operations efficiently. The real differences increasingly sit in product structure, data sync, page performance, multi-market operations, and publishing agility.

Why does product-data structure now affect paid acquisition efficiency and AI distribution directly?

Because ad platforms, merchant systems, and AI discovery surfaces increasingly depend on product data that is readable, syncable, and comparable. If title, attributes, variants, availability, price, and landing-page structure are unstable, platforms struggle to understand the catalog and struggle to deliver it efficiently.

Why does the platform affect off-site acquisition cost, not just site-building speed?

Because the site determines landing-page speed, conversion flow, tracking quality, content support, and product-sync reliability. In practice, the platform influences not only how fast a team can publish, but also whether incoming traffic can be converted, measured, and improved economically.

How should a brand choose between one global storefront and regional storefronts?

If language, pricing, payment methods, tax logic, delivery expectations, and media strategy already differ materially by market, regional storefronts usually support growth better than one global site. If those differences are still limited, one storefront may be enough for now. The real test is whether market variation has started to hurt conversion or operating efficiency.

Which foundational capabilities should matter most when evaluating an ecommerce platform in 2026?

Start with five checks: support for regional operations, strong structured product data, maintainable content and SEO workflows, reliable distribution paths into ads and commerce surfaces, and alignment between backend data and the customer-facing site. Good templates still matter, but they should not outrank those foundations.